[gtranslate]

[gtranslate]

Summarize and analyze this article with:

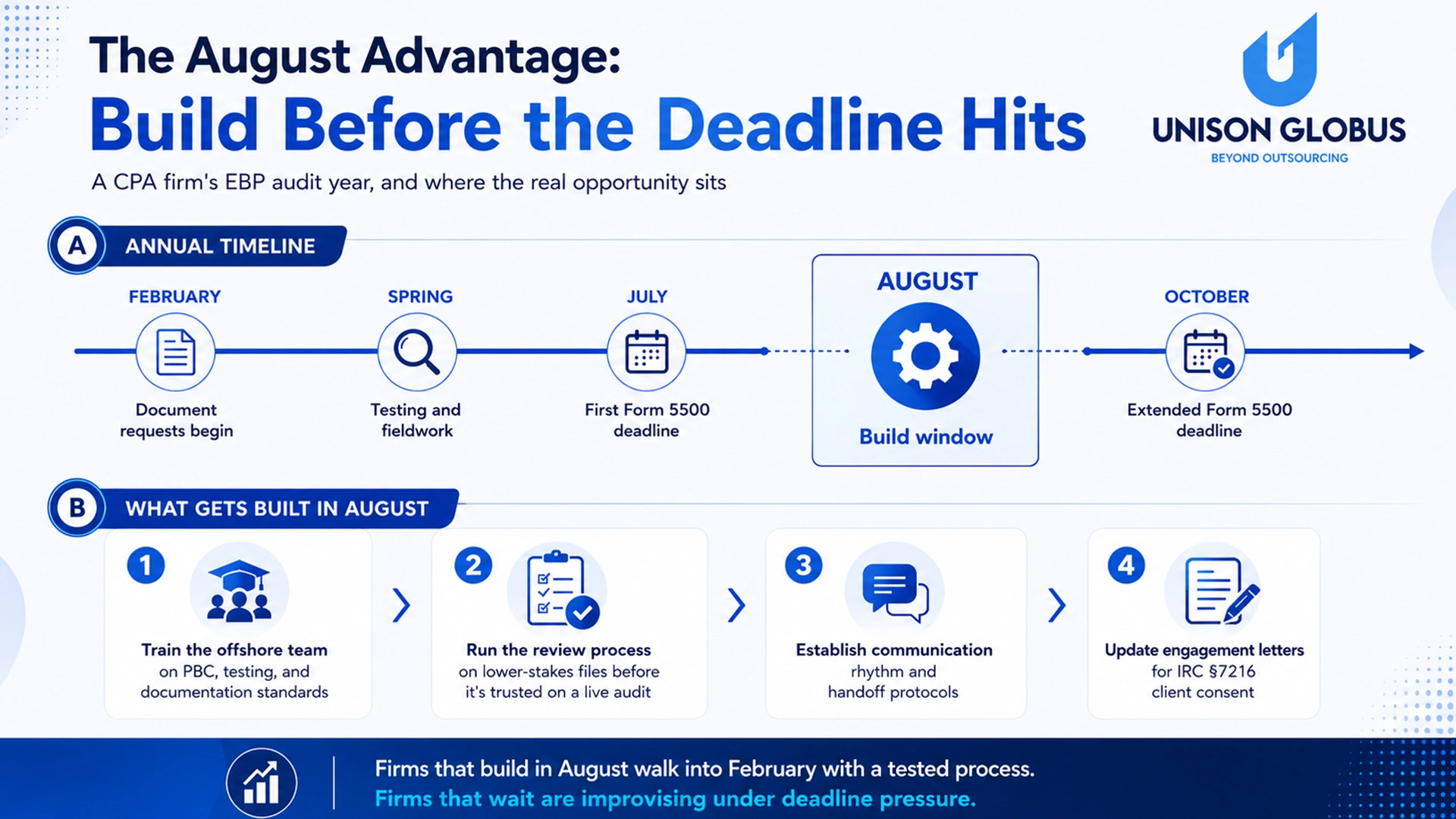

Ask any CPA firm that handles Employee Benefit Plan audits what their year feels like, and the answer is usually some version of “fine until it isn’t.” Spring brings the document chase. July brings the first Form 5500 deadline. Then, for a few weeks in August, the phone stops ringing, and the inbox slows down, before October brings the second deadline for firms that filed an extension. Most firms treat that August stretch as recovery time. Catch up on email, take a vacation, regroup before the next plan year’s paperwork starts arriving in February.

That instinct is understandable, but it wastes the one window in the calendar where a firm actually has the bandwidth to look at its Employee Benefit Plan (EBP) Audit Support process honestly. Not while a client is waiting on a draft report. Not while a reviewer is buried in testing. In August, there’s room to ask harder questions: where did the last cycle bog down, what kept getting flagged in review, and where did the firm rely on one overworked person to catch problems a better process should have caught earlier.

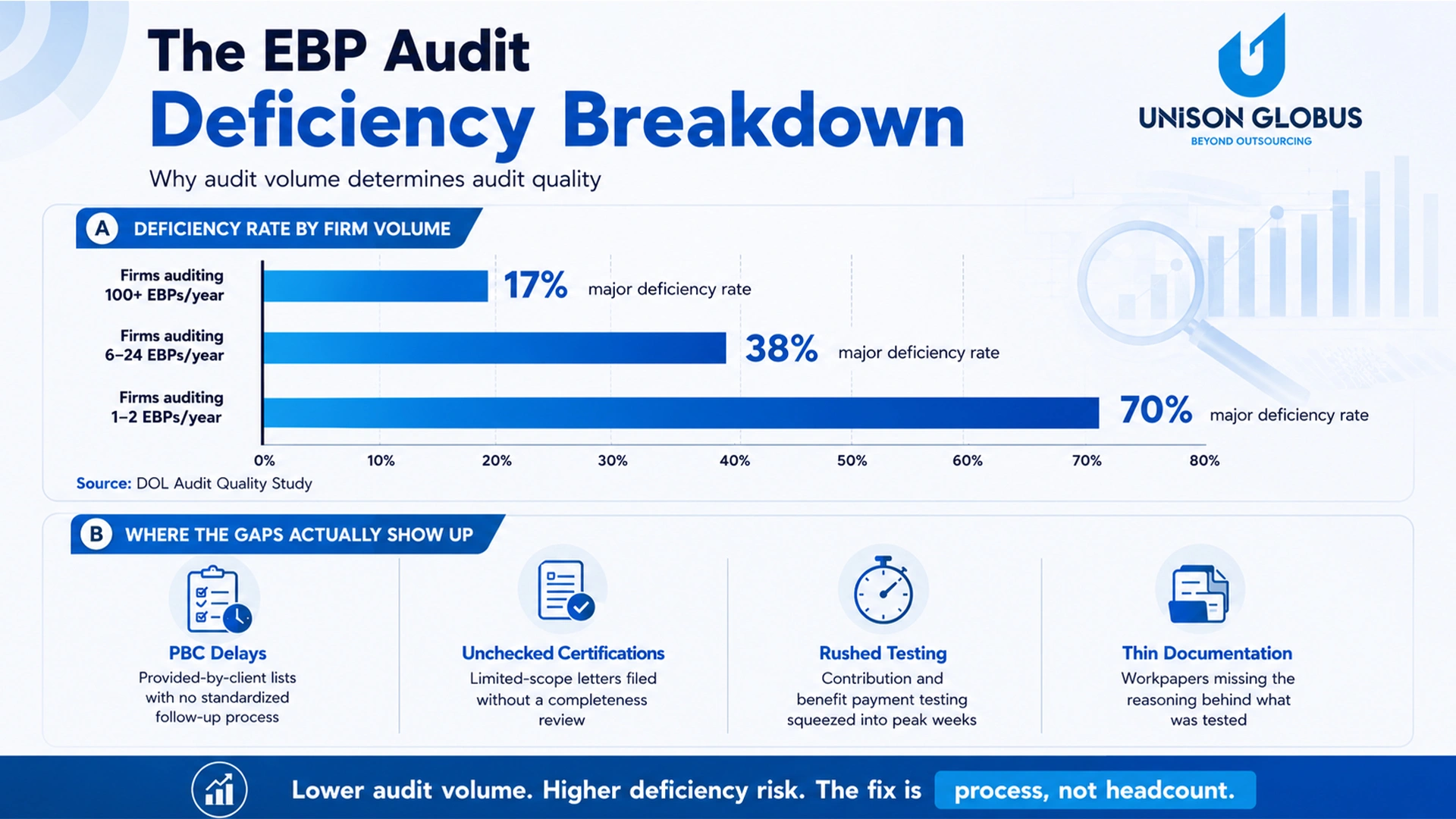

Those questions matter more in EBP work than almost anywhere else in a CPA firm’s practice, because the margin for error is thinner and the regulatory scrutiny under ERISA is sharper. The DOL’s most recent Audit Quality Study found that 30% of employee benefit plan audits contain one or more major deficiencies, and that 70% of audits performed by firms handling just one or two plans a year fall into that same category. A gap that goes unaddressed in August doesn’t stay quiet. It resurfaces in February as a missing PBC item, in June as a rushed testing schedule, and in October as a deficiency letter nobody saw coming.

This blog looks at what those gaps usually look like and why CPA firm EBP audit outsourcing, brought in during the quieter months, tends to hold up better once peak season hits.

Where Employee Benefit Plan(EBP) Audit Support Gaps Actually Show Up

“Audit gap” sounds abstract until you’ve sat through a peer review that flags the same three things every firm seems to struggle with: testing that didn’t go deep enough, contribution and benefit payment procedures that were rushed, and documentation that doesn’t fully back up the work performed. None of these are exotic failures. They’re the kind of thing that happens when a firm is moving fast and a senior reviewer doesn’t have the hours to look closely enough.

A few patterns show up again and again in firms offering Audit & Assurance Services for CPAs without a dedicated EBP specialty:

- PBC lists that drag on for weeks: Getting a complete, accurate, provided-by-client list out of a plan sponsor is often the single biggest source of delay. When a firm doesn’t have a standardized process for chasing this down, the entire engagement timeline shifts later, leaving less room for actual testing.

- Limited-scope certifications that get accepted without a second look: A certification letter from the plan’s custodian is supposed to be reviewed for completeness, not just filed. Skipping that step is a quiet way deficiencies creep into ERISA audit support work.

- Testing schedules built under time pressure: Contribution testing and benefit payment testing both require a level of detail that’s hard to maintain when one reviewer is covering five engagements at once during peak weeks.

- Thin documentation trails: Workpapers that explain what was tested and why hold up under peer review. Workpapers built in a rush, with the reasoning left out, don’t. This is one of the easiest gaps to prevent when there’s time to build a checklist instead of relying on memory.

The common thread isn’t a lack of knowledge. It’s a lack of hours, and that shortage isn’t going away on its own. Only 6% of accounting and finance leaders say they currently have the talent they need for their highest-priority work, and unemployment in the field sits at roughly 2 percent, meaning most of the people who could fill that gap are already employed somewhere else. For firms providing 401(k) audit support services, that math doesn’t leave much room to simply add another reviewer before next season starts.

This is the part of the picture that makes August worth taking seriously: every one of these gaps is fixable with planning, but only if the fix happens before the workload returns.

Curious what offshore EBP audit support could take off your team's plate this season?

Closing the Gaps with Employee Benefit Plan Audit Outsourcing

Once you can name the gaps specifically, the fix stops being vague too. Each pattern from the last section has a direct counterpart in how a well-run Employee Benefit Plan audit outsourcing arrangement is structured. This is less about adding headcount and more about adding a layer of dedicated capacity an in-house team doesn’t have room to build on its own.

- PBC management gets a dedicated owner: Instead of a senior reviewer chasing documents between other engagements, an offshore team can own the PBC list end to end, tracking what’s outstanding and flagging missing items early enough to matter. Offshore teams working overnight can have completed work waiting for the in-house team the next morning, turning a multi-day back-and-forth into an overnight cycle.

- Certifications get reviewed, not just filed: A trained offshore Employee Benefit Plan (EBP) Audit Support team checks limited-scope certification letters against the plan’s investment data as a standard workflow step, rather than something that gets skipped once the engagement gets busy.

- Testing gets the hours it needs: Offshore EBP audit services can run contribution and benefit payment testing in parallel with the in-house team’s other work, instead of squeezing it into whatever time is left during peak weeks. The work still gets reviewed and signed off by the US team, but it isn’t rushed to fit around five other engagements at once.

- Documentation becomes a built-in habit, not an afterthought: Firms that build outsourcing into their process typically standardize workpaper templates and run them through layered review before anything reaches the US team. A structured offshore delivery model puts work through self-review, a senior peer review, and a final US-side check, with error rates tracked weekly, rather than caught after the fact in a peer review.

None of this is theoretical anymore. The AICPA’s National Pipeline Advisory Group has pointed to the talent shortage as a direct cause of financial reporting delays across US businesses, and roughly 80% of accounting firm executives say they plan to increase their use of offshore teams over the next three to five years, according to a 2025 William Blair survey.

This is also where offshore audit support for CPA firms earns its place specifically in ERISA audit support work, where judgment requirements are higher and oversight is stricter than in most other outsourced accounting functions. The firms getting this right aren’t handing off audit opinions or Expert CPA Audit Services. They’re handing off the volume work, testing prep, documentation assembly, and PBC tracking, so the in-house team’s limited hours go toward review and judgment instead of data entry and follow-up.

That’s the version of CPA firm EBP audit outsourcing worth setting up in August, while there’s time to train the offshore team and work out the kinks before the next cycle starts. It’s also how firms turn a single outsourced engagement into a repeatable part of their broader audit & assurance solutions, ready well before 401(k) audit support services are needed again.

What Has to Be True Before an Offshore Team Touches a Live File

Outsourcing in an ERISA engagement raises a fair question before a comfortable one: what’s actually allowed to leave the building, what does it cost, and what does a client need to be told? Four things have to be settled before Employee Benefit Plan audit outsourcing works.

Where the line stays: AICPA independence standards separate staff augmentation, where outsourced staff perform procedures under the firm’s direction and review, from management functions, which can’t be delegated regardless of where the provider sits. An offshore EBP audit services team can prepare testing schedules, assemble documentation, track PBC items, and flag exceptions. Risk assessment, materiality decisions, and signing the opinion stay exclusively with the engagement partner. Every file coming back is a draft for review, run through the same self-review, senior peer review, and final US-side check the firm already uses in-house.

What has to be secure: Plan data includes SSNs, account balances, and beneficiary information, higher-sensitivity than a typical financial statement audit. Before any engagement letter is updated, confirm the provider has SOC 2 Type II reporting, encryption in transit and at rest, a documented retention policy, and role-based access controls. These belong in the same August planning window as training, and they’re usually the first thing a peer reviewer asks about.

What sponsors need to hear: Satisfying IRC §7216 consent requirements is one thing; a sponsor actually understanding that an overseas team will touch their plan’s data is another. Most sponsors aren’t troubled by offshore audit support for CPA firms, they’re troubled by learning about it after the fact. A short, proactive conversation confirming partner supervision and the security controls above usually turns this into a non-issue.

What it costs, and what it’s worth: CPA firm EBP audit outsourcing is typically priced well below the fully loaded cost of a US senior associate, and since EBP capacity needs are seasonal (roughly 12–16 weeks a year), cost scales with actual volume instead of carrying a full-time load year-round. The harder number to quantify is the cost of a deficiency: re-performed procedures, extra partner hours, and repeat-offender exposure with the DOL. The right comparison isn’t offshore cost against zero, it’s offshore cost against the deficiency rates already cited.

What this looks like in practice: Firms that do this well start August with a quick audit of last cycle’s deficiencies and turn that into the offshore team’s training curriculum, built on the firm’s own templates. The team then runs two or three closed, lower-stakes files through the full review hierarchy before touching anything live. By February, they’re already working inside the firm’s process, not learning it under deadline pressure. Firms that skip this end up doing the same onboarding anyway, except now it’s competing with live deadlines, which is exactly the trade-off 401(k) audit support services are meant to avoid.

The Cost of Waiting Until February

Every firm reading this already knows what February looks like. Document requests start landing, the same reviewers who were stretched thin last cycle are stretched thin again, and there’s no time to fix anything, only to get through it. Whatever gaps existed last year are still there, waiting for the workload to expose them again.

The honest picture here is more complicated than “the pipeline is collapsing.” New CPA exam candidates hit a record low of just 27,994 in 2024, the fewest since NASBA began tracking in 2008, but first-half 2025 data showed 16,448 new candidates, suggesting a real rebound toward pre-2024 levels. The pipeline is recovering. What isn’t recovering as fast is the staffing already inside firms today. Industry data shows the average share of staff holding an active CPA license at accounting firms fell from 56.0% in 2020 to 48.4% in 2024, dropping below half for the first time, and the ratio is even lower at large firms.

That’s the gap firms are actually managing through this year and next: not a pipeline that will never refill, but a workforce that’s thinner right now than it’s been in years, with the recovery still a few years from showing up on engagement teams. Treating that gap as a problem to figure out fresh each February means absorbing the same crunch every cycle. The alternative is building Employee Benefit Plan audit outsourcing into the firm’s process before the workload hits, not after.

Why August Is the Right Time to Make the Move

That’s exactly why August matters. Every benefit of outsourcing depends on the offshore team and the in-house team actually knowing how to work together before a live file lands on either desk, and that’s not something built in a week.

Onboarding isn’t instant, and treating it like a plug-and-play fix is usually where firms run into trouble. Firms that have gone through the process consistently name training as the top challenge, citing the extended onboarding period, offshore staff needs, and the difficulty of finding time for domestic staff to do that training when everyone is already busy. What a slow month actually allows a firm to build:

- A shared way of working, not just a handoff: Before anyone touches a live file, the in-house team can walk an offshore EBP audit services team through how the firm actually operates: where PBC requests get logged, how testing schedules are structured, what a finished workpaper is supposed to look like. That groundwork is what makes the relationship feel like an extension of the team rather than a vendor waiting for instructions.

- A review process that’s been run a few times before it matters: Structured offshore delivery models are typically built around layered review: self-review, senior peer review, and a final US-side check, with error rates tracked over time. That rhythm needs a few practice cycles on lower-stakes work before it’s trusted on a live ERISA audit support engagement.

- Comfort with a new rhythm of communication: Time zone handoffs, file-sharing protocols, and who to flag when something looks off all take a few rounds to feel natural. Working that out in August means nobody’s learning it for the first time while a client is waiting.

- The paperwork that has to happen before any data moves: IRC Section 7216 requires explicit client consent before any tax- or return-related data is shared with a third-party provider, including an offshore provider. Hence, engagement letters need to be updated in advance. That’s a conversation worth having with clients in a quiet month, not buried in a February intake call.

None of this is about flipping a switch in August and being fully scaled by September. It’s about using the slow season to lay the foundation for CPA firm EBP audit outsourcing, so that when document requests start arriving for the next plan year, the 401(k) audit support services team isn’t being introduced to the firm’s process. They’re already working inside it. A firm that waits until the cycle is underway ends up training a new team and running a live audit at the same time, which is exactly the kind of pressure that produces the deficiencies covered earlier, and exactly what strong offshore audit support for CPA firms is meant to prevent.

What changes year to year isn’t the deficiency risk or the staffing pressure behind it. What changes is whether a firm uses its quietest month to get ahead of that reality or spends it waiting for next season to arrive. For firms ready to build CPA firm EBP audit outsourcing, offshore EBP audit services, and 401(k) audit support services into how they actually operate, August is the month that the decision gets made.

The Window Is Open Now

August won’t last. By the time document requests start arriving in February, the firms that spent this stretch building Employee Benefit Plan audit outsourcing into their workflow will be running a tested process. The ones that didn’t will be improvising under the same pressure that produced the deficiencies covered earlier.

Unison Globus works with CPA firms to build that capacity ahead of time, with offshore EBP audit teams trained on a firm’s specific PBC, testing, and documentation standards before peak season ever starts. Our Audit & Assurance Services also help accounting firms across North America strengthen audit quality and expand engagement capacity year-round. If your firm is ready to close this year’s gaps before next year’s deadlines arrive, talk to Unison Globus. .

Ready to build EBP audit capacity before next year's deadlines hit?

Frequently Asked Questions

Yes, fully. Offshore staff work under the engagement partner’s supervision and review, the same as any in-house associate. Every conclusion, judgment call, and signature stays with the US team, regardless of how much of the underlying work is handled through Employee Benefit Plan audit outsourcing.

Requirements vary by state and by the nature of the engagement, and some boards require specific disclosures around outsourced procedures. Firms should confirm current requirements with their state board and legal counsel before finalizing any CPA firm EBP audit outsourcing arrangement, since this is jurisdiction-specific and changes over time.

For tax- or return-related data, IRC Section 7216 requires explicit, documented client consent before that data is shared with any third-party provider, onshore or offshore. Engagement letters should be updated to reflect this before any file moves to an offshore EBP audit services team.

A documented retention and deletion policy should specify how long data remains on the offshore provider’s systems and confirm secure deletion once the engagement closes. This should be agreed upon and documented before the engagement begins, not addressed after the fact, as part of any offshore audit support for CPA firms arrangement.

Most firms see a meaningful difference between a team trained for a few weeks on practice files in a quiet month versus one introduced mid-cycle. There’s no fixed timeline, but the August-to-February runway is what most firms use to get an Employee Benefit Plan (EBP) Audit Support team comfortable before live engagements start.