[gtranslate]

[gtranslate]

If you thought year end accounts filing UK 2026 would follow the same rhythm as previous years, think again. The rules haven’t changed dramatically – but the infrastructure has. The CATO portal is gone. Identity verification is now mandatory. Companies House fees went up. And the penalty clock hasn’t slowed down for any of it.

To put that in perspective: Companies House issued £157.2 million in late-filing penalties in 2024/25, across 297,682 filings – with 75,062 double penalties hitting repeat offenders. (Source: Companies House Annual Report 2024-25)

If your firm is still running the same filing workflow as last year, there’s a decent chance you’ve already got a gap you haven’t spotted yet.

This isn’t a repeat of the general compliance checklist we’ve covered before. This one is specifically about what’s changed – the deadlines, the new moving parts, and how outsourced year-end accounts services are helping firms manage the extra load without burning out their teams.

What's Actually Changed for UK Accounts Filing in 2026

Three things shifted this year that directly affect how accounting firms manage client filings.

1. CATO and WebFiling for accounts – both gone

Two free filing routes closed on 31 March 2026. The CATO joint filing portal (running since 2011) allowed accounts and corporation tax returns to be submitted together in one go – that’s gone. And separately, the Companies House WebFiling service for annual accounts has also permanently closed.

From 1 April 2026, year end accounts filing UK 2026 means Companies House and HMRC submissions must be handled separately through commercial software. Historical filings are also no longer accessible through either portal – so clients who hadn’t downloaded their records before the cutoff have lost access.

On top of that, all annual accounts must now be submitted in iXBRL format – the software handles the tagging, but firms need to confirm their tools are iXBRL-compliant

2. Identity verification is now mandatory

Since November 2025, identity verification is required for all new directors, PSCs, and LLP members. Existing directors and PSCs have until November 2026 to complete verification – but as one source notes, your actual deadline may be much sooner, depending on when your next confirmation statement is due. For firms managing large client portfolios, tracking verification status across multiple entities adds a real layer to the usual year-end accounts preparation and filing workflow.3. Companies House fees increased – February 2026

| Filing Type | Old Fee | New Fee |

|---|---|---|

| Digital incorporation | £12 | £100 |

| Confirmation statement (digital) | £13 | £50 |

| Confirmation statement (paper) | £40 | £110 |

And one to watch – April 2028

The UK Government has confirmed that accounts filing reforms set out in the Economic Crime and Corporate Transparency Act 2023 will go ahead from 1 April 2028. This includes mandatory commercial software filing for all companies and a requirement for small companies and micro-entities to file profit and loss accounts. It’s not 2026 – but firms advising clients on UK accounts filing requirements should be flagging it now.Year End Accounts Filing UK 2026 - Deadline Quick Reference for Accounting Firms

One of the most common pressure points for accounting firms isn’t missing a deadline – it’s losing track of which deadline applies to which client. Here’s a clean reference by company type.

| Company Type | Companies House Deadline | CT600 to HMRC | CT Payment (Small Co.) |

|---|---|---|---|

| Private limited company | 9 months from year-end | 12 months from year-end | 9 months + 1 day from year-end |

| Public limited company | 6 months from year-end | 12 months from year-end | Varies |

| Newly incorporated (first accounts) | 21 months from incorporation | 12 months from year-end | 9 months + 1 day from year-end |

| Dormant company | 9 months from year-end | N/A | N/A |

| Confirmation statement | Within 14 days of the review period end | N/A | N/A |

| Worked example — 31 March 2026 year-end | |

|---|---|

| Obligation | Deadline |

| Companies House accounts filing | 31 December 2026 |

| CT600 submission to HMRC | 31 March 2027 |

| CT payment (small company) | 1 January 2027 |

| Confirmation statement | Within 14 days of the review date |

Struggling to keep up with the 2026 filing changes?

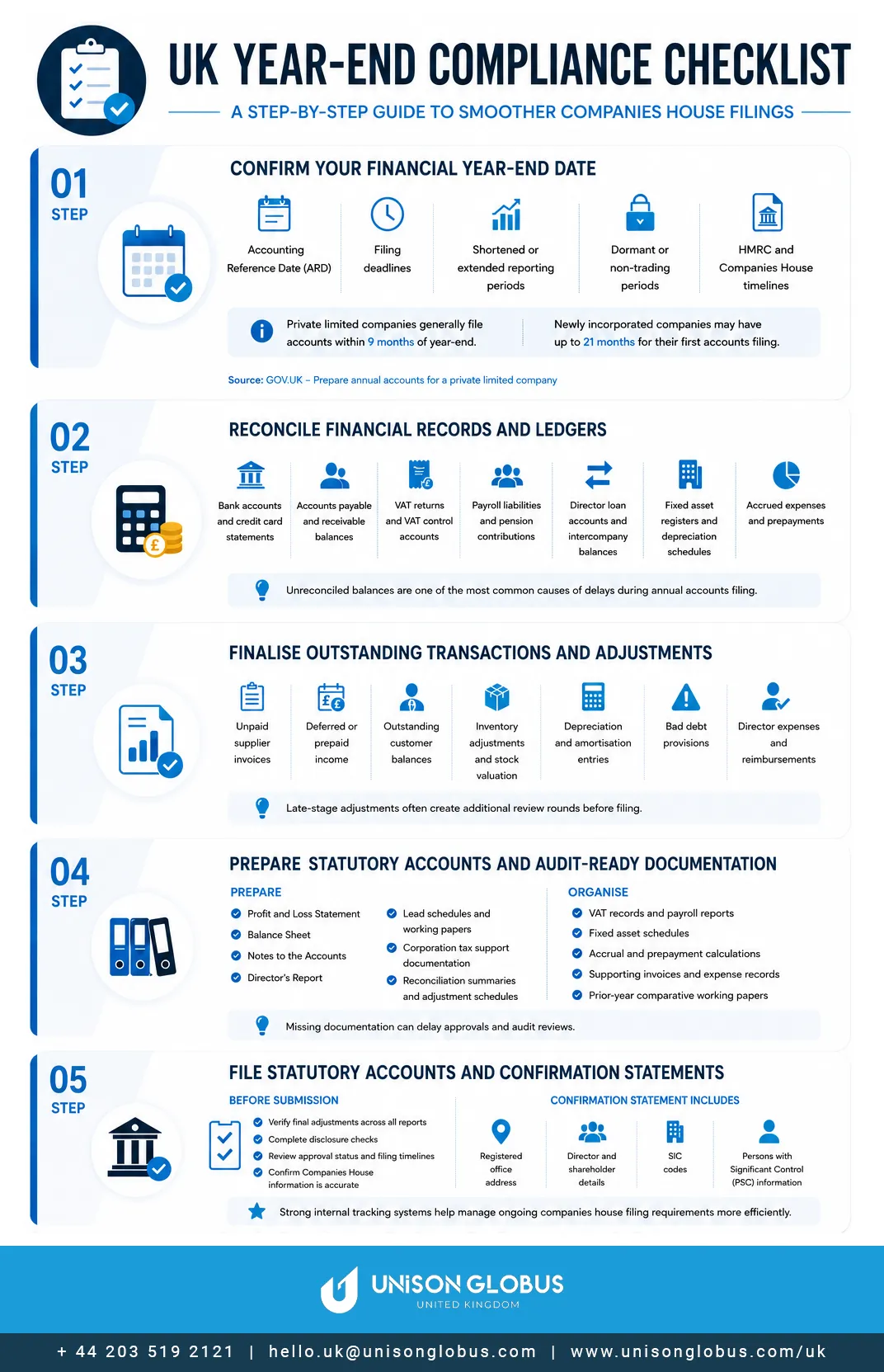

The 2026 Year-End Accounts Compliance Checklist for UK Accounting Firms

Phase 1 – 90 Days Before Year-End

- Confirm ARD and filing deadline for each client entity

- Flag any clients previously using CATO who haven’t confirmed their commercial software transition

- Check iXBRL compatibility of your current filing software

- Verify identity verification status for all directors and PSCs (November 2026 deadline is closer than it feels)

- Begin reconciliation schedules: bank, VAT, payroll, intercompany

Phase 2 – 30 to 60 Days After Year-End

- Complete all reconciliations and year-end adjustments

- Prepare draft statutory accounts under the correct standard:

| Standard | Applies To |

|---|---|

| FRS 105 | Micro-entities (turnover ≤ £632k, balance sheet ≤ £316k, ≤10 employees) |

| FRS 102 Section 1A | Small companies (turnover ≤ £15m, balance sheet ≤ £7.5m, ≤50 employees) |

| Full FRS 102 | Larger or more complex entities |

- Build working papers and lead schedules

- For FRS 102 Section 1A clients with periods beginning on or after 1 January 2026, check all three new mandatory disclosures are in templates:

- Dividends declared and paid or payable during the period

- Related party transactions – all material transactions now, not just those not at arm’s length

- Going concern – now a formal mandatory note, not just encouraged

- Note: the new disclosures also apply to prior year comparatives – not just the current period

- Coordinate director approval and sign-off

Phase 3 – Filing and Submission

- File annual accounts with Companies House via approved commercial software (iXBRL format – WebFiling is gone)

- File CT600 with HMRC separately via commercial software (CATO is gone)

- Submit confirmation statement – verify SIC codes, PSC register, director details, and UI codes for any directors appointed since November 2025

- Log all filing confirmation reference numbers

- Archive supporting documentation

The Late-Filing Risk Profile for UK Accounts Filing Requirements Has Changed in 2026

The penalties themselves haven’t changed. What’s changed is how easy it is to fall into them.

The CATO closure and WebFiling shutdown have introduced a genuine process gap for firms that haven’t fully transitioned. It’s not negligence – it’s workflow confusion during a software migration. A firm that previously managed Companies House and HMRC as one combined submission now has two separate processes to track per client. Multiply that across a portfolio with staggered year-end dates, add the FRS 102 Section 1A disclosure changes, adding preparation time, and the identity verification tracking overhead, and the margin for error is thinner than it’s been in years.

One thing worth flagging to clients: late filing penalties are charged to the company, not the director personally – but the legal responsibility sits with the director. And Companies House appeals are accepted only in genuinely exceptional circumstances. A software transition doesn’t qualify. Firms offering year-end accounting solutions should be building these transition risks into their client communication now, not after a deadline is missed.

How Outsourced Year-End Accounts Services Help Firms Manage the 2026 Shift

The case for outsourcing isn’t new. But the reasons it makes sense in 2026 are specific.

- The CATO transition created extra work nobody budgeted for. What was previously one submission is now two tracked workflows per client. For firms managing 100+ year end accounts filing UK 2026 deadlines, that’s a meaningful capacity addition without any corresponding increase in fees or headcount.

- The FRS 102 Section 1A changes mean accounts take longer to prepare. More mandatory disclosures, comparative information requirements, and client conversations around dividend visibility all add time to what used to be a straightforward statutory accounts UK deadline preparation process.

- Identity verification tracking is operationally intensive. Monitoring UI codes and verification status across a large client portfolio – before each confirmation statement is due – quietly consumes senior staff time that should be going elsewhere.

- Peak filing months create real capacity ceilings. September to December is brutal for firms with March year-end clients. Scalable year-end accounting solutions mean you’re not turning away work or de-prioritising clients during your busiest window.

- Outsourced teams absorb the prep work, not the responsibility. Your firm retains review, sign-off, and client relationships. Our outsourced year-end accounts services handle preparation, coordination, and documentation – fitted around your existing workflows.

That’s exactly what we do at Unison Globus UK. We work with UK accounting firms as a dedicated outsourced partner, plugging into your process where capacity is tightest – whether that’s preparation, reconciliations, or keeping track of filing deadlines across a large client portfolio.

If you’d like to see how it works before committing, we offer a free trial so you can evaluate the quality of our work firsthand. Fill in the contact form and one of our team will be in touch to understand your setup, your peak period pressures, and where we can best support you.

Ready to take the pressure off your next filing season?